Monthly Letter: November Update

12/15/2024

Market strength continues with some bumps – ready for the post-election phase

As we move through the month of November, equity markets remained positive year-to-date, with the volatility that started late summer becoming less pronounced (with some recent exception as explained below). For the month of October, the markets were down slightly in advance of the election with the S&P 500 down 1.0%, the tech-heavy Nasdaq down .52%, and the slower growing companies of the Dow Jones Industrials down 1.3%.

Through the close of November 15th, the S&P 500 was up 24.5%, the Nasdaq up 21.2%, and the Dow Jones Industrials up 15.3%.

The much anticipated election is over

The presidential election is finally over, with Donald Trump emerging victorious. President Trump’s market friendly views, including less regulation and lower taxes, helped drive positive markets on the 6th, with the S&P 500 up 2.5%, the Nasdaq up 1.5%, and the Dow Jones Industrials up a stronger 3.6%.

Market strength continued, albeit at a slower pace, in the days past the election with some notable speculative trading in cyber-currency related areas.

We view current equity markets as positive with the backdrop of continued strong earnings growth, the progression of a Fed rate cutting cycle, and a market friendly administration.

October economic data

The Bureau of Labor Statistics (BLS) released the October CPI report on November 13th. The headline CPI rose by 2.6%, which was worse than the prior month’s 2.4% number. The month over month number was .3%, excluding the volatile food and energy components, same as last month. While that number was higher than expected, the market reaction was initially muted and many investors remained hopeful for another 25 basis point cut in December. This CPI report followed a Fed meeting on November 7th, in which the Fed funds rate was cut 25 bps to a 4.5-4.75% level. Inflation numbers have come down notably this year and the Fed rate cut cycle is in motion, although the outlook for steady cuts in 2025 is uncertain at this point.

The BLS also reported unemployment numbers on November 1st. October job growth was only 12,000 new jobs vs. 233,000 added jobs in September and 78,000 more in August (both the September and August numbers were revised down). The market did not panic over fears of a hard landing recession scenario as had happened in July. Some of the weakness was attributed to the hurricanes and the Boeing strike. Wage growth slowed from the prior month to .4% year-over-year versus 4.0% in September, and the unemployment rate stayed flat at 4.1%. While these numbers were weaker than in prior months, they too did not give pause to the market.

Earnings – the third quarter was a success

Earnings season is mostly over, with over 93% of the companies in the S&P 500 having reported actual results for the third quarter. Of these companies, 75% have reported actual EPS above estimates and aggregate growth was 5.4%. As previously mentioned, in the prior quarter aggregate earnings were up 10.8%, a solid print and above expectations. Earnings growth expectations for the full year are projected to be 11% in 2024.

On the horizon – keep on the lookout for inflation

No sooner had the Fed declared victory over inflation than concerns resurfaced. Did the Fed start the cutting cycle too soon? Is the economy running too hot? And now a new worry – will President Trump’s tariffs increase inflation?

Generally, all three of the questions remain to be seen. Likely, a monetary “hawk” would not have cut rates by 50 bps in July. However, the jobs report has shown some weakness both in jobs created and in wage growth, so the Fed would argue that they are trying to get ahead of a slowdown. The economy is strong with GDP growth at 3.0% in the second quarter, but given pockets of weakness and a stretched consumer, many would argue against the economy being too hot.

As for tariffs, how they end up getting used is uncertain. Widespread adoption across all imports likely will involve congressional approval, making heavy cost tariffs less likely. Overall, tariffs and their use is something we will be watching and analyzing closely, but presently the market is not pricing them in as a negative.

Overall, markets sold off a bit in the second week of November, mostly on inflation worries. At this point, it is too early to conclude inflation will reignite, but again it is a factor we are watching closely.

To Sum Up

We believe the market can continue to perform well and that the new pro-business and pro-market administration will ultimately be favorable to company earnings, which should benefit the market. We also believe our portfolios are solidly diversified and well-positioned for varying economic scenarios including a higher for longer rate environment.

The market volatility that started this summer has picked up post-election and we continue to view periods of volatility as a normal part of the market. That said, we feel that equity returns going forward will continue to be attractive. We have incorporated the relatively full equity valuations into our analysis and exercise care as we build out portfolios.

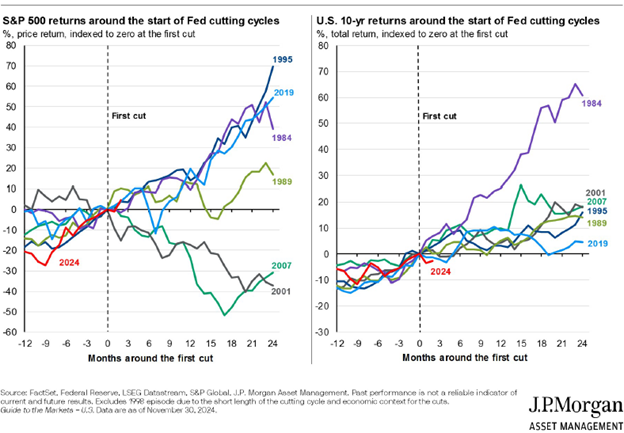

The rate cut cycle has started and traditionally the period during a Fed rate cut cycle provides a tailwind to upcoming equity market returns. For fixed income investors, rates still remain higher than in prior years, although expected yields will come down as rates come down. As rates continue to come down, moving to higher yielding alternatives will likely continue to make sense in our view.

Overall, our team continues to focus on the vast array of economic statistics, market events, and company earnings as we make our way through the last part of 2024.

Sources: JP Morgan Asset Management, Bureau of Economic Analysis, Bureau of Labor Statistics, Morningstar, Factset, Slickcharts, Yahoo Finance, and Ycharts

Disclaimer

GoalVest Advisory is a SEC registered investment adviser. Information presented is for educational purposes only intended for a broad audience. The information does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and are not guaranteed. GoalVest Advisory has reasonable belief that this marketing does not include any false or material misleading statements or omissions of facts regarding services, investment, or client experience. GoalVest Advisory has reasonable belief that the content as a whole will not cause an untrue or misleading implication regarding the adviser’s services, investments, or client experiences. Please refer to Form ADV Part 2A the adviser’s ADV Part 2A for material risks disclosures. Past performance of specific investment advice should not be relied upon without knowledge of certain circumstances of market events, nature and timing of the investments and relevant constraints of the investment. GoalVest Advisory has presented information in a fair and balanced manner. GoalVest Advisory is not giving tax, legal or accounting advice, consult a professional tax or legal representative if needed.