Unlocking the Magic: Structured Growth Notes in Action

12/11/2024

What are Structured Growth Notes?

Structured growth notes are customized financial products designed to meet specific investment objectives by combining traditional fixed-income elements with exposure to an underlying asset. They offer unique payoff structures, potential for enhanced returns, and some level of downside protection, making them a compelling option for investors seeking tailored solutions.

Learning Terms and Mechanics with a Real Example

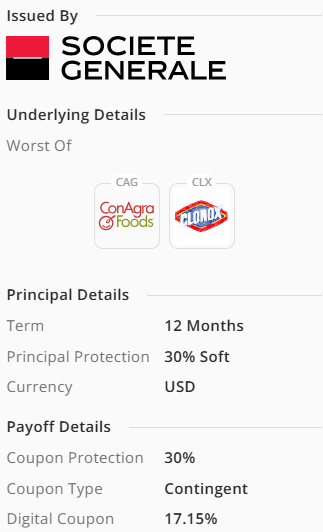

Underlier

The underlying assets (underliers) are the key determinants of the note's performance. In this example, the structured note is linked to ConAgra Foods (CAG) and Clorox (CLX) using a "Worst Of" structure. This means the performance of the note is based on the worse performing of these two assets over the investment term.

Maturity

Maturity refers to the duration of the investment, typically ranging from one to five years. Investors are generally expected to hold structured notes to maturity, although some may include embedded call features, allowing the issuer to redeem the notes early under certain conditions.

In this example, the maturity is 12 months, meaning the potential final payout occurs after one year. Gains from structured notes held for more than one year are often treated as long-term capital gains, which may have favorable tax implications.

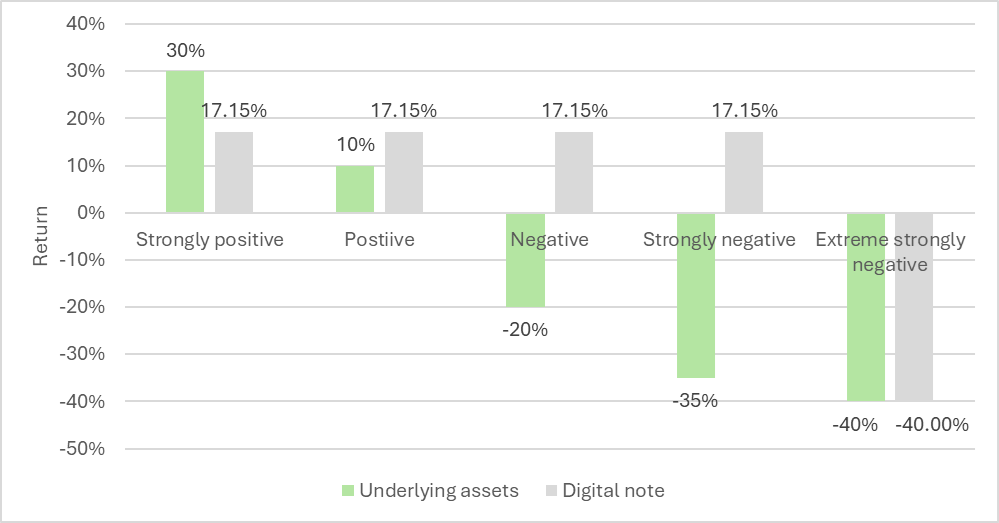

Expected Payoff at Maturity

The payoff at maturity is contingent upon the performance of the underlying assets. For this note:

If neither ConAgra Foods nor Clorox falls below the 30% coupon protection level, the investor receives a 17.15% digital coupon in addition to their principal.

However, if either asset breaches this protection threshold, the investor’s principal is reduced in proportion to the underlier's performance.

Protection

Structured notes often include a buffer or soft protection to mitigate downside risk. This example includes 30% soft principal protection, shielding the investor from losses as long as the worst-performing underlier does not decline by more than 30% from its initial price at maturity. If this threshold is breached, the investor is fully exposed to the losses of the worst-performing underlier.

Why Should Structured Growth Notes Be Part of a Portfolio?

Enhanced Return/Yield Potential

Structured notes can potentially offer higher returns compared to traditional fixed-income products, especially in a low-yield environment.Customization

These notes can be tailored to align with specific market views, risk tolerance, and income requirements.Diversification

Including structured notes in a portfolio adds exposure to different payoff structures and risk-return profiles.Downside Protection

Features like soft protection and buffers help reduce risk, making them attractive for cautious investors.

Risks

Market Risk

The performance of structured notes is tied to the underlying assets, which are subject to market volatility.Liquidity Risk

Structured notes are generally illiquid, making it difficult to sell before maturity.Credit Risk

Since structured notes are issued by financial institutions, their repayment depends on the issuer’s creditworthiness.Complexity

Understanding the terms, mechanics, and payoff scenarios of structured notes requires careful attention to detail, as their complexity can lead to misinterpretation of risks and returns.

Structured growth notes can be valuable tools for sophisticated investors looking to enhance returns and manage risk. By understanding their mechanics and potential outcomes, investors can make informed decisions about integrating them into their portfolios. Always consult a financial advisor to determine suitability based on individual goals and circumstances.

Disclaimer

The information presented should not be considered personalized investment, financial, legal, or tax advice. This notification is not an offer to buy or sell, or a solicitation of any offer to buy or sell, any of the securities mentioned herein. Certain statements contained herein may constitute projections, forecasts, and other forward-looking statements, and are based primarily on assumptions applied to certain historical financial information. Certain information has been provided by third-party sources, and although believed to be reliable, it has not been independently verified, and its accuracy or completeness cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this document and are subject to change. Past performance is not indicative of future performance. Principal value and investment return will fluctuate. There are no implied guarantees or assurances that the target returns will be achieved, or objectives will be met. Future returns may differ significantly from past returns due to many different factors. Investments involve risk and the possibility of loss of principal. The values and performance numbers represented in this report reflect management fees. The values used in this report were obtained from sources believed to be reliable. Performance numbers were calculated by Black Diamond using the data provided by your custodian. Please consult your custodial statements for an official record of value.

The securities involve risks not associated with an investment in ordinary debt securities. Selected Risks Associated with any of these structures include: - Notes are not principal protected and investors can lose some or all their initial principal if the underlying asset falls below the Principal Barrier Level. - Contingent coupon payments. Investors may not receive periodic interest payments if the performance of the underlying asset falls below the Coupon Barrier Level. It is possible that investors will not receive any coupon payments over the life of the Note. - Potential for early redemption and reinvestment risk. Notes will be automatically called if the performance of the underlying asset is at or above the Initial Strike Price on the defined Observation Date. If called, investors may not be able to reinvest their proceeds in a product with a comparable coupon. - Returns are limited to the coupon payments, if any. Investors will not participate in any price appreciation of the underlying asset. Additionally, investors will not receive dividend payments generated by the underlying asset. - Limited secondary market. Notes should be considered buy-and-hold investments and investors should hold them to maturity. They are not traded on an exchange and there may be little to no secondary market available. - Issuer credit risk. Notes are senior, unsecured debt obligations of the issuer and all payments of income and principal are therefore subject to the creditworthiness of the issuer. - Complex investments. Notes may have complex features and may not be suitable for all investors.